With an astonishing revenue growth in 2016 and 2017, SharedLabs, Inc. (SHLB) is the next unicorn startup company that will sell shares in Wall Street. The company��s growth is sustained by innovative services in exciting sectors, such as artificial intelligence, blockchain, and the Internet of Things. Also, SHLB is growing as a result of ambitious acquisitions, such as iTech US, Inc., and SmartWorks, LLC.

Source: S-1

BusinessHeadquartered in Jacksonville, Florida, and founded in 2016, SharedLabs is an information technology services company. The company describes its services with the following words in the prospectus:

��We enable businesses and organizations to radically adapt as they harness our extensive experience with next-generation technologies like cloud hosting, big data analytics, artificial intelligence (��AI��), blockchain and the Internet of Things (��IoT��). Rather than offer a ��one size fits all�� approach, through strategy, consulting, design and implementation, we tailor our professional services to each client��s needs to provide customized IT solutions, allowing them to make the absolute most of our services.�� Source: S-1

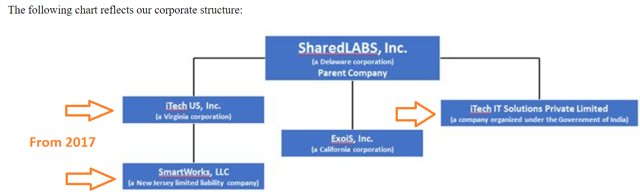

SharedLabs consists of a group of five companies. The parent company, SharedLabs, Inc., is based in Delaware and controls four companies, which are headquartered in the United States and India. Have a look at the following figure and note that both iTech US, Inc. and SmartWorks, LLC, were acquired in 2017. The exponential growth of SharedLabs is best explained by the acquisition of these two entities:

Source: S-1

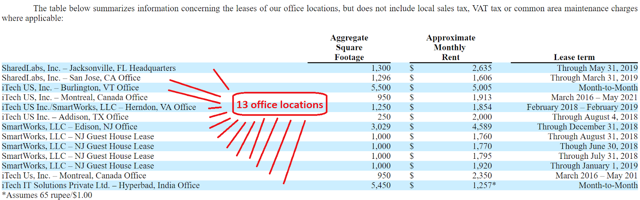

Before checking the financial figures, let me show what the company has achieved in only two years of existence. First of all, the group has five entities, but the number of office locations is more significant. I could count 13 office locations in the United States and India. Check out the following table:

Source: S-1

What��s more interesting is the number of employees, which, in my view, really shows the exponential growth of SharedLabs. In the last two years, the company has gone from no employees to, as of May 15, 2018, 550 employees all over the world. Doesn��t sound like an incredible story?

What��s the market opportunity?According to the March 2017 report published by The Business Research Company (Source: S-1), the IT services industry in the United States is expected to grow at a compound annual growth rate (CAGR) of 5.1%. That said, the market is also very large. In 2020, its total value is expected to be $1,163 billion.

How is the growth in the industry sustained? That��s the most interesting. The report noted that advancements in AI and IoT are driving the demand in this market. Bearing in mind that SharedLabs is mainly focused on providing these services, I believe that the company should exhibit growth at a higher rate than the IT sector.

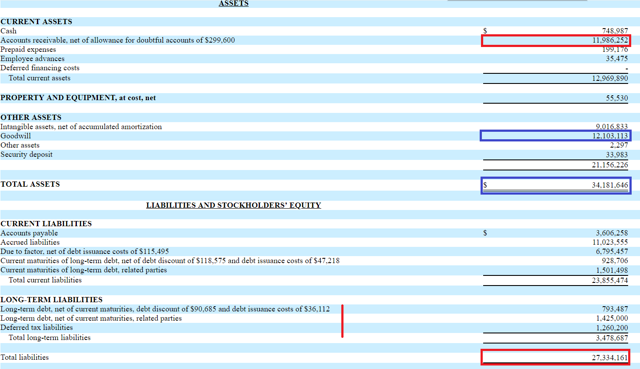

Financial Statements - The acquisitions, goodwill and intangiblesTaking into account that SHLB did not exist three years ago, the cash and asset generation is quite impressive. As of December 31, 2017, the total number of assets was equal to $34.18 million with $12.10 million in Goodwill and $9.01 million in intangible assets:

Source: S-1

You should have assumed that the Goodwill accumulated is from the acquisition of iTech US Inc., and its subsidiary SmartWorks, LLC, which we mentioned above:

Source

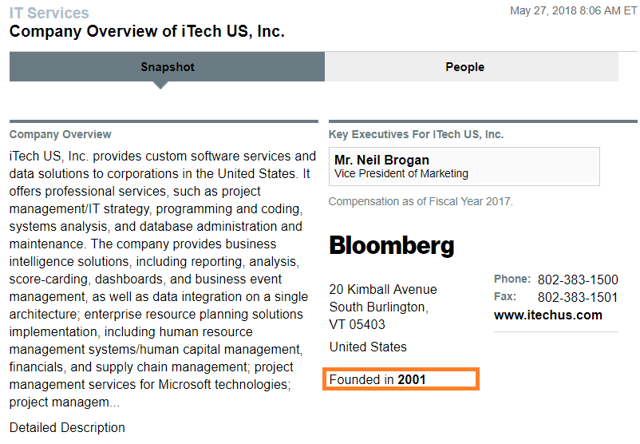

Are you interested in this disruptive acquisition? You need to know that iTech US, Inc. was founded in 2011 as shown by Bloomberg, and the business objective was similar to that of SharedLabs:

Source: Bloomberg

The company had large amount of employees, which considered the iTech a good place to work:

Source: LinkedIn

Source

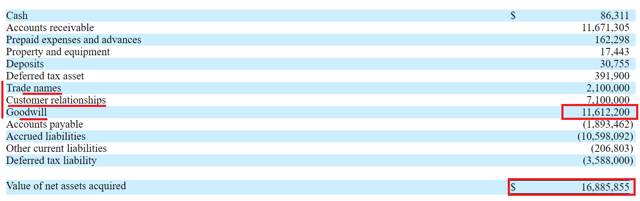

The total value of the net assets acquired was equal to $16.885 million. They mainly consisted of $11.612 million in goodwill, trade names for $2.1 million, and $11.671 million in accounts receivable:

Source: S-1

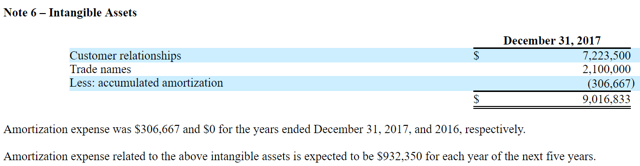

Please note that the trade names and the customer relationships are the intangible assets that were shown in the balance sheet of SharedLabs. They have obviously suffered amortization in 2017 as shown in the following figure:

Source: S-1

How did the company pay for iTech? That��s another interesting feature. Like it happens in most acquisitions of emerging startups, iTech stockholders received a combination of cash, long-term debt, and warrants to purchase stock of SharedLabs. The following is the information that you need to know:

Source: S-1

Finally, I also need to mention that Exoi S, Inc. was also acquired in exchange of 149,067 shares of the company��s common stock. This amount of stock was said to be worth $711,285 in the prospectus:

Source: S-1

What��s my take? With three companies acquired in 2017, the company��s growth, undoubtedly, could not be explained without mentioning these transactions. Investors interested in this company need to really comprehend these acquisitions to assess the real value of each common stock of SharedLabs.

Taking into account the amount of money paid for Exoi S and iTech, we can use the following calculation to get an implied valuation of each share. SharedLabs acquired Exoi S and paid with 149,067 shares. The fair value of the stock issued was $711,285, which implies that each share is equal to $4.77. The company is selling shares at $5 in the IPO, which does not seem an absurd price given the amount paid for Exoi S.

That said, I need to raise the following concerns about the way SharedLabs is growing since it will affect the stock price. So far, the growth has been fueled by several transactions. The number of employees and business opportunities have exploded up, which has been welcomed. However, in the future, SharedLabs will not be able to acquire three companies per year. Thus, bear in mind that the growth will not be as remarkable in the near future. Additionally, if the acquisitions don��t really work out, the goodwill and the intangible assets will be diminished, which could lead to a reduction in the amount of net assets.

To sum up, be sure to revise the integration process and the goodwill in the balance sheet. The stock price will go up or down depending on these two features.

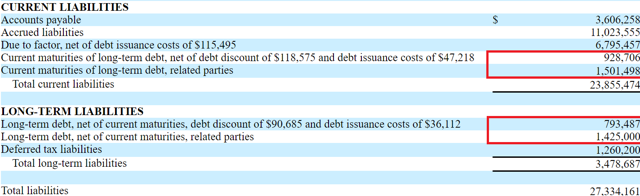

Financial statements - Liabilities and debtAs of December 31, 2017, SharedLabs exhibited $27.33 million in total liabilities, including approximately $4.6 million in debt as shown in the table below:

Source: S-1

The debt includes a business loan acquired to finance the acquisitions noted. This business loan was for total principal of $2 million plus interest at an annual rate of 20% for total interest of $0.8 million. While I don��t appreciate this term, I believe that if the company continues growing at the same pace, the interest expenses could be paid. The following is what you need to know:

Source: S-1

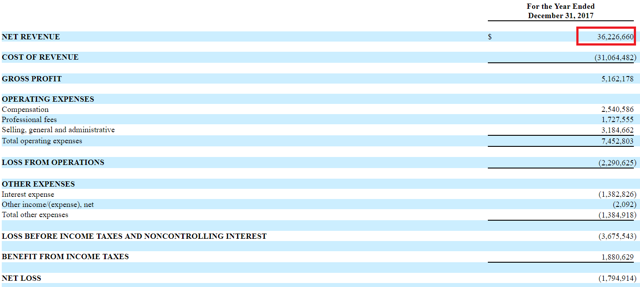

RevenuesTaking into account that the company did not exist in 2016, I believe that the revenue growth is astonishing. As of December 31, 2017, net revenue was equal to $36.22 million, and the gross profit accounted for approximately $5.1 million. While the net loss was equal to $1.79 million, I don��t believe that the investors will really care about it. This is an emerging company, and what really matters is the revenue and cash growth. The following is the income statement as provided in the prospectus:

Source: S-1

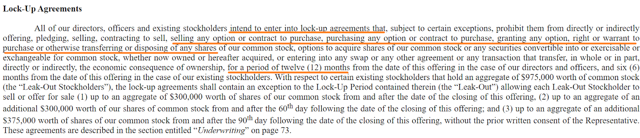

Lock-up agreementsAnother very relevant feature that I will study closely is what insiders and directors do with their shares. If they commence to sell shares right after the IPO, which I expect to start in June, I will not be a buyer of this name.

Please note that the prospectus noted that the directors ��intend�� to enter into lock-up agreements that prohibit them from selling shares for a period of 12 months from the date of this offering:

Source: S-1

ConclusionWith an impressive and aggressive acquisition strategy, SharedLabs seems to be growing at a large pace, which, in my view, will seduce many investors. That said, I am not right now a buyer of the shares. I want to see how the company integrates the companies acquired before acquiring shares.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.